As we enter the second week of the new year, I thought it would be appropriate to revisit my post on budget basics. I still clearly remember the shock to the system that going to one income caused me. Luckily my dear husband is very sorted when it comes to the finance department. We did have to make lifestyle changes to enable me to stay at home and they did take some getting used to. No flash holidays, buying clothes on sale, etc but the best thing for me was setting a family budget and then tracking our daily expenditure. It is amazing how much you can spend in a week without realising it.

*****

The New Year is a great time to revise the family budget and set new goals for the family finances. We have been running a family budget since we went to one income about seven years ago.

Over these years we have developed a comprehensive excel spreadsheet for the family budget. I do have to credit Mr Infrastructure as the “brains” behind the spreadsheet and the simple process that we follow.

To help with this post, Mr I modified our family budget spreadsheet to demonstration amounts and altered some of the categories of expenditure in the spreadsheet to be more generic and easily understood.

Click here to see the Planning With Kids Family Budget Spreadsheet.

We follow a 3 step process to set and then track the family budget. Each step has its own corresponding spreadsheet:

STEP 1- REGULAR PAYMENTS SPREADSHEET

The aim with this spreadsheet is to input all known payments that you will have through out the year. The previous year’s bills can be used to approximate what you might spend for bills that are of a variable nature.

By calculating the total regular payments you have through out the year, you can then use this figure to help determine what your discretionary expenditure can be.

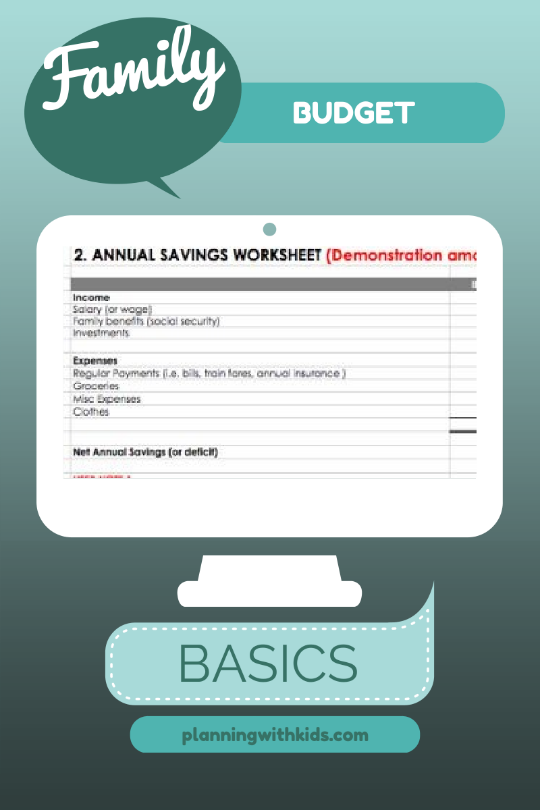

STEP 2- ANNUAL SAVINGS SPREADSHEET

This is a basic income minus expenditure spreadsheet. You enter all the sources of income and their frequency that you are likely to receive throughout the year, to arrive at a total income figure.

For expenses, the regular payments total from the first spreadsheet is automatically linked as the first expenditure item. For the next three expenditure items you need to estimate how much you will spend on each category – Miscellaneous items, Groceries and Clothes. The spreadsheet currently works on a weekly figure, but this can be easily changed if you prefer to work on fortnightly or monthly amounts.

Once you have entered these estimates, the spreadsheet then calculates what your net annual savings (or deficit) will be with that level of expenditure. It is at this point when you have put your first estimates in that you may have to make revisions to achieve your financial goals for the year.

For some families the goal may be to balance the budget and therefore you will be happy if this amount is $0. For other families if you are saving for a deposit for a house or for a new car, you may need this figure to be $10,000 surplus to meet your savings goal.

STEP 3- INPUT OF SPEND SPREADSHEET

This is where you track on a daily basis the amount you spend on the discretionary categories (Miscellaneous items, Groceries and Clothes) in reality. As Mr I writes in his notes on the spreadsheet:

“Be disciplined…input every expenditure when it happens (including those sneaky little credit card purchases or $3 coffees).”

It is amazing how quickly all those little expenditures add up! The great thing that I have found about using the spreadsheet regularly to track our family budget, is that it does make me think twice on those impulsive purchases. Sometimes I do just go ahead and splurge at a sale, but usually only if I know that there is room in the budget to do so.

As the budgeted figures are weekly you need to be mindful that it is not always appropriate to run a zero balance. For example, although the allocation for clothing in the demonstration spreadsheet is $100 a week, this is not how in reality expenditure on clothes works. A new suit for Mr I to wear to work would be multiple times this amount, but bought only a couple of times a year. To do this without putting the budget into deficit, we need to build up a surplus in the months before hand.

Putting The Family Budget On Google Docs

Until recently, Mr I would tell me his expenditure and I would update the family budget spreadsheet daily when I was online. However, this wasn’t as effective as I would have liked. A couple of months ago I uploaded the family budget to Google Docs, shared access with Mr I and now we both have access to the family budget online. We can both update the spreadsheet ourselves from anywhere we have internet access.

I have written a tutorial on how to load documents on to Google Docs on my Set Up Email Address blog – Google Docs: Managing Your Family Budget. This will show you step by step, with screen shots how simple it is to have greater access to your family budget online.

I have uploaded the family budget spreadsheet to Google Docs and set access to “Share With The World”:

I would love to know if you run a budget and do you track your daily expenditure?